By Patrick Imam

Developing countries are struggling to mobilise resources to finance social and infrastructural development. The author argues that one avenue is to tax luxury goods more heavily, which could simultaneously tackle inequality and spur development with minimal distortionary effect, as was practiced by many successful East Asian countries in the past.

INTRODUCTION

Since the Global Financial Crisis, the risks posed by rising inequality have become ever more evident. Not only are some academics blaming the global crisis on rising inequality, but also the shallow recovery is attributed to the inability of lower and middle-income families to spend more (Stiglitz, 2013).

In the context of Lower Income Countries (LICs), where extreme inequality has always been present, the problems are compounded by fiscal strains in the context of enormous social and infrastructural needs. While LICs have done tremendous advances since the 1990s, the gap to be filled to reach decent lives for the majotrity of their citizens is still gaping.

To simultaneously combat rising inequality, and generate growth, some economists have proposed some sort of wealth tax, with the proceeds to be used by the government to raise social and infrastructural spending (e.g. Piketty, 2013). The argument is that high-income households, who have a lower propensity to consume than middle and low-income households, reduce aggregate demand. However, while appealing in theory, taxes on wealth have not been very common in practice, unlike taxes on the two major tax bases – income and expenditure. Most countries in the world use income taxes and expenditure taxes (e.g. VAT, custom, excises). Wealth taxes, are extremely rare, and where they do exist, account for relatively small amounts of total tax revenue (typically less than 1 percent).

The problems of administrating a wealth tax are significant in practice, preventing it from being a more prevalent source of government revenue:

• Disclosure: It is easy to hide many forms of wealth, whether physical ones like diamonds, or keep assets overseas, particularly for the local elite.

• Valuation: A wealth tax is not easy to administer: information is limited, much of the wealth is held in assets that are difficult to value (not marked-to-market). In addition, given the narrow base of such a tax, the revenue potential is limited.

• Liquidity Concerns: Many households – particularly older ones – that are asset rich are liquidity poor, making it harder to tax them without forcing them to sell their part of their assets.

• Capital Flight: Imposing a wealth tax in the context of mobile capital has become extremely difficult, especially in developing countries, where much of the wealth of high net worth individuals is held abroad. If rich countries like Sweden – with an effective tax administration – has abolished the wealth tax in 2007, it is because the resulting capital outflow was so much larger (by a factor of 300 according to some studies) than the tax revenue raised. The magnitudes may be even higher in LICs.

• Impact on Growth: A risk from a wealth tax is that it discourages investment, as the rewards to risk-taking are diminished.

• Political Economy Constraints: In many countries, the richest have the means and influence to impact the political discourse, and to lobby politicians to act in their interests, by limiting the revenue impact of a wealth tax.

Empirically, recent academic research has also suggested that many countries are at the peak of the “Laffer Curve”, with higher level of taxation of wealth leading to lower tax revenue for governments, at least in OECD countries (see Gruner et al., 2014). In developing countries, the issue would be less the level of a wealth tax, and more the inability to administer such a tax.

Therefore, while the case for a wealth tax is questionable in practice, until now, there has been, surprisingly little that has been written about the effect of taxing luxury consumption, as a proxy for a wealth tax. Such a tax would act as a “substitute” for a wealth tax, as it would target mostly conspicuous consumption carried out in large part by high net worth individual.

The case in favor of taxing luxury is not new. Among early economists, the case for luxury taxation, which was often made on moral grounds, has been mentioned at least since the work of John Stuart Mill in Principle of Political Economy published in 18481 (Mason, 1998 provides a good summary of the debate among social scientists about the merits of taxing luxury goods).2

The reason economics have not taken the subject of taxation of luxury goods more seriously, despite tax systems implicitly taxing luxuries differently from necessities, is twofold. First, luxury consumption, by accounting for a small part of the economy until recently, is not deemed to be important enough to be considered an important source of revenues. Second, because of the difficulty of defining luxury goods, it is inherently difficult to quantify its effect (See Box 1).

BOX 1: Definition of Luxury Goods

Defining “luxury” is not easy as it can cover many meanings. Sometimes, it is used to denote anything that is not strictly necessary to life or to cover a minimal standard deemed adequate by society (Mason, 1998). This definition is, however, vague, as what might be considered a luxury in one country, might be considered a necessary good in another one. In fact, the definition of luxuries across time is neither constant across countries, nor across time (see also Chang, 1997).

For instance, while bananas were considered normal goods in West Germany in the 1970s and 1980s, they were considered luxuries in Eastern Germany. It was often the case that relatives from the West, when they would visit their families in the East, that they would bring bananas as a gift. Thus there is a relativity element when it comes to luxury consumption. One person’s luxury can be another person’s normal good.

Similarly, the definition of luxuries changes across time. When the mobile phones became available in the late 1980s, they were clearly considered luxuries in developed and developing countries. Nowadays, because they have become so affordable, most people, even in developing countries would not consider them as luxuries, but rather as normal or even necessary goods. Cars and travel appear in the current context to be the largest share of luxury according to various studies.

The first advantage of a luxury tax is not only that it generates revenues, and may do so at lower political or economic cost than alternatives such as income taxation. The second motivation is that the demand for luxury products is likely to be inelastic for high net worth individuals, meaning that the distortionary impact is likely to be contained. Luxury goods are often positional goods, goods that are desired not because of their intrinsic property, but because they compare favorably with other similar goods. The third motivation – in Emerging Markets (EM) and LICs in particular – is that a luxury tax may discourage consumption that individuals might over-consume in the absence of taxation, and may reduce imports, save foreign exchange, and encourage higher domestic savings or domestic consumption, as luxuries are mostly imported in LICs/EMs.

Some economists (see Eltis, 1984) have argued that particularly in the early stages of development, where income inequalities are very high, that luxury taxation would be very effective in promoting economic development. As the rich in developing countries spend a disproportionate amount of their money on luxuries, they forgo savings that could be used for domestic investment, thereby reducing growth. The current account in developing countries will also be improved if a developing country imports fewer luxury goods (given their high import content), thereby leaving more foreign exchange to import intermediate and other investment goods (Nurkse, 1953, UNCTAD 1997). Finally, luxury consumption, which by definition can be forgone, as it is not a necessity, might also be politically easier to tax and could be an effective way to collect tax revenues.3 While the case could be made that developing countries could borrow abroad to finance domestic investment, evidence suggests that capital does not flow easily across countries (Feldstein and Horioka, 1980).

This idea has until now, however, had a limited impact on the economic profession, even among development economists. Only during periods of extreme stress, such as the Second World War, has this policy of restricting luxury consumption been used continuously by policymakers. In the context of a war economy, a distinction was made between necessities and luxury goods, with the latter being rationed or taxed heavily such as to provide more resources for necessities. After the war, when shortages stopped, the distinction was eliminated again (Chang, 1997). More recently, countries such as India have introduced extra taxes on luxury cars.

Similarly, following the first oil shock of 1973, one of the key decisions taken by governments in Europe was to tax oil consumption heavily, a good that was not a pure necessity, as it could be forgone by using public transportation. Particularly in Europe, several arguments were used to tax oil consumption more heavily, from reducing its environmental impact and encourage the development of alternatives to tax luxury goods, and thereby encourage public transportation instead of car usage.

LUXURY TAXATION AND POTENTIAL IMPACT ON ECONOMIC DEVELOPMENT

While this idea has not been much analysed within academic circles, the taxation of luxury goods might have been one of the sources explaining the growth diversion between successful Emerging Market economies in East Asia and less successful ones such as Latin America and Sub-Saharan Africa, with the former having higher tax levels on luxury goods than the latter ones. Clearly, the superior performance of some countries over others cannot simply be explained by different taxes, as development is a multi-dimensional problem. However, taxation of luxuries is helpful in explaining part of the story.

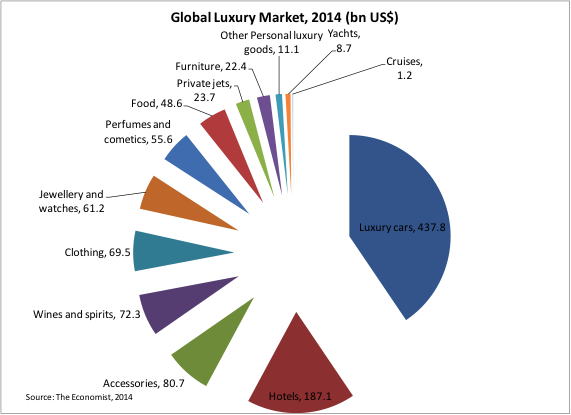

To minimise this definitional problem, the focus is on goods that would be treated as luxury goods in most contexts, both across time and across countries. While goods like caviar, perfume, expensive jewelry and watches would be considered luxury items in most countries, they do not account for much in terms of economic significance, and scant statistical data is available for them. As a result, we look at factors such as ownership of passenger cars and foreign travel instead, which account for large shares of GDP in many countries, even in poor ones. They are good proxies to analyse luxury consumption that cannot be purchased by many people in developing countries. Moreover, data on car ownership is more readily available than most other forms of luxury goods.

Anecdotal evidence on how highly luxury goods have been taxed throughout the world is easily available. “In the recent past, for example … Algeria imposes a 150% tax on caviar. Indonesia’s luxury tax and import tariff on passenger cars of more than 3000 cc engines amount to 50% and 80%, respectively” (Ikeda, 2006, p. 495). Similarly in Japan, in the initial post World War II period, goods considered to be luxurious such as golf clubs were taxed as much as 100 percent (see Chang, 1997). In Egypt during the 1980s, it cost twice as much to go from Cairo to a foreign capital such as Brussels on a return flight, than it cost to go on a return flight from Brussels to Cairo, with the same carrier. The Egyptian government used different tax rates for tickets purchased domestically from those purchased abroad. This policy aimed to discourage Egyptians from going abroad, thereby encouraging rich domestic Egyptians to spend their income domestically, thereby keeping the money in the domestic economy, while encouraging foreigners to visit the country.

Given that few countries have an explicit “luxury tax”, typically, luxury goods are subject to different taxes across countries. In some countries, they are subject to a high VAT, while in others, they will be subject to a high excise tax, while in others, they might be subject to a combination of taxes. It was not possible to find systematic data on levels of taxation of luxury goods across countries, with4 the exception of the US Department of Commerce (see Table 1 above), which has only compiled the data for 2006. This has limitations, as it is focused on a single year, and does not include all countries.

The table does provide evidence that taxation of car imports was as a whole higher in Asia than in other developing countries. Instead of using tax data, an equivalent way of looking at the suppression of luxury goods was to see the amount of cars.5 America is used as a benchmark case. While this variable has the disadvantage of not looking at taxation directly, it still has the advantage of giving a clear indication of whether luxury consumption is suppressed or not, which is likely to be highly correlated with taxation of luxury goods. While not all of the suppression can be attributed directly to high taxation, as it could be due to trade control (through foreign exchange rationing) or credit control policies, the use of taxes is still likely to have been the most important determinant of keeping luxury consumption low.

Table 2 (see Table above) provides us with information on car ownership for a selected group of countries for which data is available throughout the period (this draws on Chang, 1997). It shows that some countries at similar levels of development had fewer cars per capita than others. The countries that stand out in having very low levels of car ownership for a given level of income are Germany, Japan and South Korea, those countries which industrialised very rapidly. For example, when GDP per capita was US$4,000 (in constant 1985 dollars) in Korea and Japan, car ownership was only 12 and 15 respectively. For other countries such as Brazil, Malaysia and South Africa, car ownership at that same level of income was closer to between 61-91 in the case of Malaysia and 64-80 in the case of Brazil.6 In other countries, car ownership has grown much faster than income. Argentina is a good example, with a stagnating income per capita at US$5,000 between 1965-1989, but with the number of cars per 1,000 rising from 41 to 133 over that period. Korea on the other hand only saw a rise in car ownership from the end of the 1980s onwards. Between 1960, when income per capita was US$1,000 and 1987 when it reached US$5,000, car ownership only increased from 1 per 1,000 people to 2 per 1,000.

Similarly in the case of other regions, we find a similar pattern, with the fastest growth taking place in the period when car consumption per capita was low for a given level of income. South Africa has seen a huge increase in the number of cars per person, despite a small growth in income per capita. A look at Turkey and Egypt suggests that following the trade liberalisation in the 1970s, car consumption relative to income growth has grown much faster. Malaysia and Thailand had higher car consumption compared to Korea at similar levels of development, but it differs significantly from Korea before it reaches a high-income level.

To conclude, in the most successful developing countries, growth in car ownership was very low relative to income until a certain level of income per capita was achieved. In fact, only when the level of about 50 percent of income relative to the US is achieved did car consumption in the more successful industrialising countries start to rise faster. Also, periods of liberalisation of trade were often associated with a rise in car consumption, but also often lower growth rates, suggesting that repressing car consumptions might have been beneficial for growth.

III. CONCLUSION

To conclude, in the current economic environment of rising economic inequality, and urgent development needs, using a wealth tax may not be the right way forward, both in developed and developing countries.

In this paper, we discussed that wealth taxes are not easy to implement and would in most countries not lead to large revenues. Instead, this paper proposes to go for a luxury goods tax, which has the advantage that it taxes mainly the consumption basket of the rich, without distorting their behavior. While further rigorous empirical evidence is needed, the paper suggests that there is evidence to suggest the hypothesis in lower income countries that taxing luxury goods could help economic development.

About the Author

Patrick Imam is a senior economist in the African department of the IMF. He has worked in the Western Hemisphere, Asia and Africa, and his research interest encompasses financial market development and financial stability. He holds a PhD in economics from the University of Cambridge.

Patrick Imam is a senior economist in the African department of the IMF. He has worked in the Western Hemisphere, Asia and Africa, and his research interest encompasses financial market development and financial stability. He holds a PhD in economics from the University of Cambridge.

References

• Chang, Ha-Joon (1997) “Luxury Consumption Control and Economic Development” Paper presented at UNCTAD

• Feldstein, Martin and Charles Horioka (1980) “Domestic Saving and International Capital Flows” Economic Journal Vol. 90, pp. 314-329

• Guner, Nezih, Martin Lopez-Daneri, and Gustavo Ventura (2014), “Heterogeneity and Government Revenues: Higher Taxes at the Top?”, CEPR Discussion Paper 10071

• Ikeda, Shinsuke “Luxury and Wealth” International Economic Review, Vol. 47, pp. 495-526

• Mason, Roger (1998) “The Economics of Conspicuous Consumption: Theory ad Thought since 1700” Northampton, MA: Edward Elgar

• Mill, John Stuart (2004) “Principles of Political Economy” Prometheus Books

• Nurkse, Ragnar (1953) “Problems of Capital Formation in Underdeveloped Countries” Oxford: Basil Blackwell

• Piketty, Thomas, 2013 “Capital in the Twenty-first Century” (London: Belknap Press)

• Stiglitz, Joseph, 2013 “Inequality Is Holding Back the Recovery,” Divided: The Perils of Our Growing Inequality, New York: The New Press, pp. 44-49.

• UNCTAD (1997) “Trade and Development Report” Geneva: United Nations

Notes

• The views expressed reflect those of the author, and do not necessarily reflect those of the IMF or IMF policy.

1. To quote Mill:“[Luxury taxes] have some properties which strongly recommend them. In the first place, they can never […] touch those whose whole income is expended on necessaries; while they do reach those by whom what is required for necessaries, is expended on indulgences. In the next place, they operate in some cases as … the only useful kind of sumptuary law … a great portion of the expenses of the higher and middle classes in most countries [is incurred] from regard to opinion, and an idea that certain expenses are expected from them, as an appendage of station; and I cannot but think that expenditure of this sort is a most desirable subject of taxation. If taxation discourages it, some good is done, and if not, no harm; for in so far as taxes are levied on things which are desired and possessed from motives of this description, nobody is the worse for them. […] it is a creation of public revenue by which nobody loses.”

2. Veblen’s (1899) “The Theory of the Leisure Class” also drew attention to the importance of luxury consumption.

3. This does not have to be the case though. In countries where the rich have a lot of political cloud, they might lobby for light taxation on luxury goods, given that they are the primary purchasers of these goods.

4. While anecdotes are easily available, there is little systematic evidence that is available on how highly taxed luxury goods such as cars or foreign travel. This problem of data availability is difficult to correct for. Neither “Taxbases” (includes Tax Notes International), nor “Foreign Tax Law” nor “IBFD Online”, the most important tax databases, have a systematic account of taxation levels across products. The one exception is data provided by the “United States Department of Commerce International Trade Administration Office of Aerospace and Automotive Industries”

5. The discussion here is focused on car ownership rather than on international travel, due to data constraints. While data on international travel is easily obtainable, there is limited information on the breakdown by residents, and it is also difficult to tax only the residents in an attempt to impose a luxury tax on them. At the same time, if a government taxes all travelers, then the tourism sector may suffer.

6. The reason we do not have a single number, but rather a range, is because a country’s per capita income stagnated, but car ownership still increased over that period.

Disclaimer: This article contains sponsored marketing content. It is intended for promotional purposes and should not be considered as an endorsement or recommendation by our website. Readers are encouraged to conduct their own research and exercise their own judgment before making any decisions based on the information provided in this article.

Payout")

Payout")

{kind=link}