By John Mellor

Responses from regulators to the failures in bank governance and standards of conduct revealed by the crisis of 2007-2008 will fall short of what is needed to restore credibility and trust in financial services. Besides regulation, a change in bank culture that embeds appropriate values and behaviours is needed. But what does this mean in practice? Research on governance and culture of banks, underway at the University of Leicester, has already identified the several key influences that bear on the “soft” issues, and which will require serious consideration by bank leaders of today and those who will assume governance responsibilities in the future.

Banking Challenges

Of the major issues that are serious concerns to banks currently, and into the foreseeable future, four stand out as critical. They are:

1. The impact of regulation on their activities;

2. The impact of technology on their operations;

3. The generation of an acceptable return on capital; and

4. The rebuilding of credibility and trust amongst users of financial services, and society at large (what might be termed ‘moral capital’).

All four issues point to a clarification of the purpose of banks and raise fundamental questions for the governance and culture of financial institutions.

Focus on Governance of Financial Institutions

Since the Cadbury Report on corporate governance in 1992, attention has been largely focussed on non-financial corporations. However, following the financial crisis of 2007-2008, the focus has shifted to shortcomings in the governance and culture (ethics and behaviours) of financial institutions, particularly banks. In due course it is expected that other financial service sectors, such as asset management and insurance, will receive closer governance scrutiny, albeit neither of those have been implicated in the 2007-2008 crises.

Whilst the crisis was largely linked to banks in the world’s developed economies, the issue of governance and culture of financial institutions is a global one, reflecting the global nature of banking and finance. Initiatives by governments and regulators in the US, UK and continental Europe have been taken, and are ongoing, to address bank governance shortcomings and to put in place frameworks to avoid financial and economic catastrophe in the future. The importance to the world economy, and society generally, of a sound and efficient banking and finance system is self-evident. In this respect, banking and finance assume a quasi-public responsibility and role that sets it somewhat apart from some other economic activity.

Committees of Enquiry Following the 2007-2008 Crisis

Conclusions on banking culture from reviews of banking governance since the financial crisis have indicated evidence of shortcomings in behaviours by practitioners leading to a breakdown of trust in banks. Most notable amongst reviews conducted in the UK and the rest of the EU are:

1. The Turner Review for the FSA (Financial Services Authority) on a regulatory response to the global banking crisis (March 2009)

2. The UK Government sponsored “Walker Report” (November 2009)

3. The Parliamentary Commission on Banking Standards Report (June 2013)

4. An EU Green Paper “Corporate Governance in the Financial Institutions and Remuneration Policies” (July 2010)

The Walker Report set out to examine corporate governance in the UK banking industry. The report covered effectiveness of risk management, board composition and effectiveness (and also of audit, risk, remuneration and nomination committees), and the role of institutional shareholders. However, Sir David Walker, the author of the report, remarked five years after its publication that, were he to be writing it today, he would include several new points. The main one of these would be the issue of banks’ culture, something almost entirely absent from the original report – “The need is not only to focus on hard risk (capital, leverage, liquidity, etc.), where the world is now in a much better place, but also to focus on soft risk or culture”.1

In its final report on banking standards – “Changing Banking for Good” – the Parliamentary Commission outlined the radical reform required to improve professional standards and culture across the industry. In the chapter devoted to governance, standards and culture, the report makes the connection between the culture of an organisation, and therefore its values, and leadership:

“The character of leadership is particularly important in ensuring good cultural values are permeated throughout financial services firms.”

Recommendations to Government included in the Parliamentary Commission Report made their way into the Banking Reform Act which received Royal Assent in December 2013.

The Regulatory Response

Regulators in Europe and the US have moved to revise and tighten the regulation of banks in response to the financial crisis. In the UK, the Vickers Report (September 2011), from the Independent Banking Commission, recommended a “ring fence” around retail banking to separate its activities from investment banking. This is enshrined in legislation in the Banking Reform Bill noted above and will take effect from 2019. Concurrently, the Bank of England has assumed new powers of banking regulation and supervision and established a new regime comprising:

1. A Financial Policy Committee (FPC) responsible for systemic risk, i.e. macro prudential supervision

2. A Prudential Regulatory Authority (PRA) responsible for oversight of safety and soundness of banks and insurers, i.e. micro prudential supervision

3. A Financial Conduct Authority (FCA) responsible for investor protection, market supervision and regulation, business conduct of banks and financial services, and civil and criminal endorsement of market abuse rules

The new regime took effect from 2012.

Whilst a revision of the regulatory framework for banks is an inevitable consequence and response to the banking crisis, it is not of itself a sufficient response if banks are to be returned to their fundamental purpose of putting their service to the economy and their clients first. This will require, in addition to a regulatory response, the establishment of a banking culture, which embodies and supports appropriate ethical values and behaviours, before trust in the banking system can be restored.

A Banking Response

In the aftermath of the financial crisis, governments and regulators have taken steps to avoid a repeat. Their work is still ongoing. In the meantime, banks have shown some inclination to improve their governance and culture, but without further progress, there is potential for another catastrophe with implications for society and economies. Restitution of a well governed and culturally appropriate banking system, operating on the basis of acceptable values and behaviours with service to clients put first, will take a considerable time.

The Banking Culture Environment

Careful study of a selection of UK financial institutions – Barclays, Lloyds, Rothschild, Schroders, Warburgs and Nationwide, representing a range of ownership and business models, reveals some insights into the complexity of factors with a bearing on culture which must not be viewed in isolation, but linked to bank governance.

Governance is the ultimate driver of a bank’s culture because an organisation’s ethos is driven from the top, namely the board of directors responsible for governance, and the setting of an appropriate culture has an important influence on decision making throughout that organisation.

It is important to keep in mind, however, that culture is not an end in itself, but that values and behaviours exhibited by financial institutions must be acceptable to the users of financial services, and society at large, for the retention of trust and protection of their franchise to allow them to operate successfully. Speaking at the second annual Inclusive Capitalism event in the City, Mark Carney2, Governor of the Bank of England, noted that the financial sector has to win over society by cutting excess and behaving in an ethical way if it is to flourish in the future.

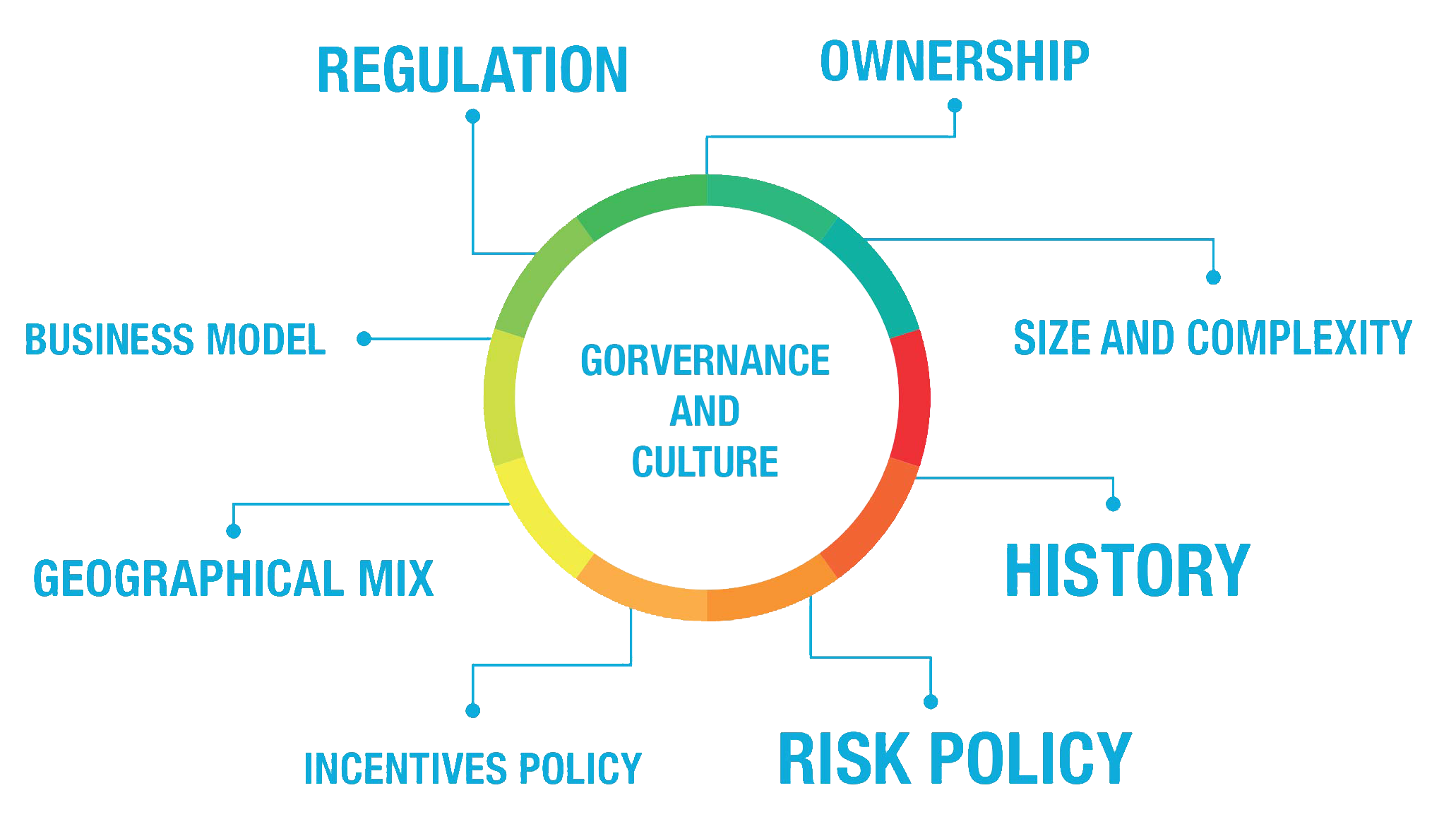

The diagram above presents a framework to explore the drivers of a bank’s culture, whilst retaining the important link with governance. Regulation is included here not in its capacity as rule setter, but as a potential influence on culture.

This framework gives rise to some of the more basic questions for banks which are included below, together with some qualifying comments.

Ownership – How does ownership influence banking culture?

Ownership can range across private partnerships, publicly listed banks and mutual organisations, each providing a different model for influence and control. In the case of publicly listed global banks with widespread institutional shareholding (pension funds, insurance companies, etc.) it is likely that there are also significant bondholders who, as major creditors, could have an influence on culture.

Corporate structure – How do different business models and geographic mix affect governance and culture?

Cultures vary across geographic and business activities. A retail banking culture is very different from an investment banking culture for example, making for difficulty in establishing a common culture. This cultural challenge, and the governance challenge arising from size and complexity, has raised implications for establishing a common culture where dominant sub-cultures exist.

Regulation – Does regulation have a role in developing appropriate culture?

Intuitively, regulation would appear to have an influence on culture, but this relationship is not sufficiently understood. Hector Sants3, in a speech to the Chartered Institute of Securities and Investment Conference, argued the case for regulation having an important influence.

History and risk – What bearing does a bank’s history have on the evolution of its culture?

Fundamental principles laid down by founders of banks define banking culture and their evolution over time can help track changes. In cases where there has been extreme deviation from acceptable values and conduct, then lessons may be learned from an historical perspective and instilled into a contemporary context. In an article on Barclays’ evolution from its Quaker roots, John Plender4 finished with – “Those Quaker bankers may still have something to teach us all.”

Incentives and measurement – How can appropriate values and behaviours set from the top be made to permeate throughout the organisation?

With a culture based on sound values and acceptable behaviours set from the top, the challenge still remains of how to instil that culture throughout the whole organisation.

The framework represents a useful beginning to examine the drivers of banking culture, values, and behaviours in particular circumstances, but research at the University of Leicester continues to accumulate a better understanding.

Conclusion

Regulation alone will not be sufficient to make the step change in banking ethics needed to address the shortcomings in bankers conduct revealed by the 2007-2008 financial crisis. This will require a focus on the “soft” issues of banking culture, that is – the restoration of sound ethics, appropriate values and behaviours. Ultimately, this is a task for bank leaders responsible for bank governance.

Within any bank there are a variety of inputs into culture and this article sets out the key ones which require serious consideration to effect the required change in banking culture to ward off any unnecessary and restrictive banking regulation.

About the Author

John Mellor is Professor of Governance in Banking and Finance at the University of Leicester and directs the University’s research project on governance and culture of financial institutions. A recognised authority in governance, he was previously an international corporate banker with Citibank and is Chairman of the Foundation for Governance Research and Education.

John Mellor is Professor of Governance in Banking and Finance at the University of Leicester and directs the University’s research project on governance and culture of financial institutions. A recognised authority in governance, he was previously an international corporate banker with Citibank and is Chairman of the Foundation for Governance Research and Education.

References

1. Arnold, M. (2014, Dec). A banking grandee’s rethink on the rules of the game. Financial Times. Retrieved from http://on.ft.com/1yzLihn

2. Griffiths, K. and Goulde, T. (2015, Jun). Mark Carney urges an ethical view of financial excess. The Times. Retrieved from http://www.thetimes.co.uk/tto/business/industries/banking/article4481257.ece

3. Sants, H. (2010, Jul). Do regulators have a role to play in judging culture and ethics.

4. Plender, J. (2012, Jul). How traders trumped Quakers. Financial Times. Retrieved from http://on.ft.com/MaXgbB

{kind=link}